Making a budget is an easy step toward meeting your financial goals, living the life that you want, and making sure your financial future is secure. Learning to budget can also help you pay off debt, freeing up your income to use toward other goals.

A good budget is your ticket to financial freedom, increased peace, and paying off debt.

I used to write articles for the newsletter where I worked. Sometimes when I was at a loss for words I would use the thesaurus to get a fresh idea.

Just for fun I looked up budget. What is a budget if not an annoying spreadsheet or a rigid rule designed to suck all the joy out of life?

Some of the results were pretty fun.

Do you know what the first result for the opposite of budget is? Debt.

A few other contenders include need, loss, scarcity, shortage, deficit, want.

But words that are interchangeable with are Allowance, funds, award, finances, ration, income, and my favorite—plan.

A budget is just a plan, which explains why it is difficult for some of us to start one—we aren’t all good at planning.

Planning is a skill and an important one. If you were going to build a house or a business, you wouldn’t skip the planning phase. In fact you might hire an expert to do it for you! You shouldn’t skip a plan for your money either. Budgeting helps you become an expert in your own money.

With that in mind, here are six key steps to making a plan (aka budget) for your money. It takes awhile to get everything in order so don’t expect it to be a perfect fit the first time around.

Budgeting is a process and it’s always in motion, the key is to start.

In a few months you’ll be on your way to a better budget!

Let’s make a budget with these six easy steps…

1. DEFINE A GOOD WHY:

This doesn’t need to be earth shattering but budgeting can be tough so it is good to get real about why you’re doing it. Maybe you want to:

- break the cycle of living paycheck to paycheck,

- save for a vacation,

- know exactly how much debt and savings you have to calculate your net worth,

- pay for school, a car, a house,

- help a loved one

I would bet anything you have a great reason to improve your financial picture. If you can’t think of any reason, you can use mine:

I want to be in control of my money so money doesn’t control me

If you ever feel like throwing in the towel—and you will sometimes—remember why you’re doing this and take another step. (you can do it!)

2. KNOW WHAT YOU OWE

Gather a pen and paper and some patience and start to list your debts if you have them. Put it all down. List loans like:

- Car loan,

- mortgage,

- student loans,

- home equity loans,

- credit cards,

- loans from family members

Don’t leave anything out. If you aren’t sure what the balances are, call and find out. If you have no debt but you still want to organize your money, list your assets—this includes all cash, checking account balances, retirement savings, change under the couch, etc…

3. CHECK YOUR CHECK

- Do you know how much you get paid and how often? The number of people who say they don’t know might surprise you.

- Do you know how much is withheld from your paycheck for taxes and is it enough? (if you owe money at tax time the answer is no).

- Do you check every time you’re paid to make sure that the hours are correct, your benefits were all disbursed, and the taxes look a-ok?

It only takes finding one mistake on a paycheck to understand the importance of this. After a few suspicious looking paychecks at a former employer, we found out that the payroll company was making a mistake with our withholding. I was able to amend my taxes and get about $2,000 back eventually, but I only caught the mistake because I was reviewing my paystub each pay period.

It’s important to look out for mistakes but knowing how much you bring home can help you make adjustments and goals, too.

Familiarize yourself with your pay. If it’s different every pay period that will present an extra challenge but it doesn’t mean you can’t budget—it just means that the budget is more important! Here are some items to verify:

- You’re withholding enough to cover taxes

- All benefits (if you have them) are correctly set up and being withdrawn

- The hourly rate is correct

- The hours worked are correct

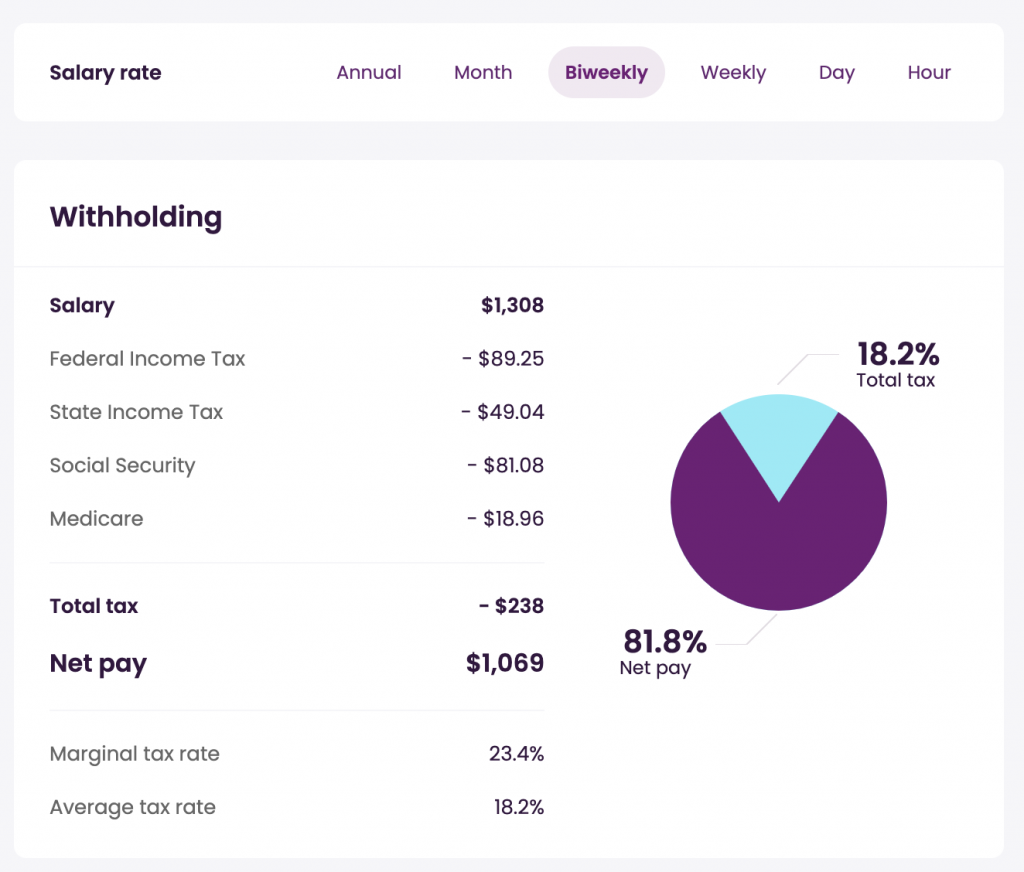

I love to use this tool to calculate what my take home pay should look like. This won’t work as well if you work on commission or as a contractor, but if you work hourly or on salary it’s great:

https://www.talent.com/tax-calculator.

Enter the amount you make, the frequency of pay, and your home state. If your paychecks don’t look similar to the net pay, make some adjustments with payroll or HR.

This tool is also great for calculating your take-home pay at potential jobs. Once you have a working budget, you will be able to calculate whether a salary offered by a company is enough to cover your expenses and goals.

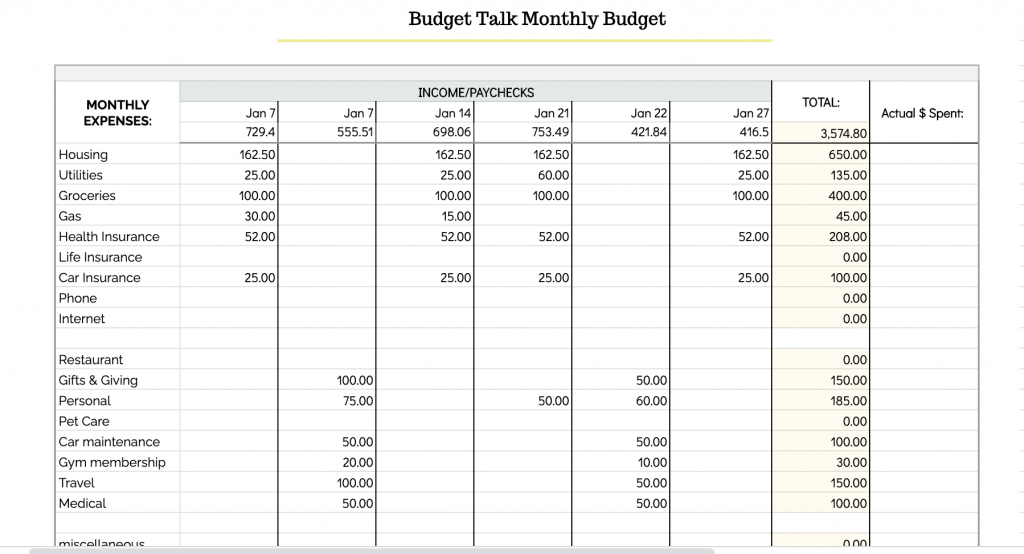

4. LIST YOUR EXPENSES

Write everything down. Don’t write down what you wish you spent on groceries, write down what you actually spend, your best guess will do for now—be very honest because you won’t do yourself any favors if you end up without enough for necessities. You can always adjust this later If you aren’t sure, you’ll start tracking expenses in step 6 to give you some useful data.

Think of all your bills and everything you need to spend money on to live your life. Once you have written all your expenses, divide them by the number of paychecks, this is how much you need to set aside from each check.

You can get as detailed as you want with this, but you want the big categories covered like:

- Housing

- Utilities

- Food

- Insurance

- Transportation

- Phone/Internet

- Medical

- Personal allowance

- Pet Care

- Gifts

If you are paid biweekly, you will divide the expenses by two, if you’re paid weekly, divide them by 4 and so on. Whatever number you come up with is what you will need to set aside that paycheck to cover expenses for the month.

5. PAY NECESSITIES—THEN PAY DEBT AND SAVE

Now that you have listed your expenses by category and you know what you need from each check, you will be able to start on your next payday! If you don’t have enough in your check to cover everything, don’t panic. Pay the most urgent bills first while you work out how to get some extra income. If you are lucky enough to pay all the bills and have some left, then you can start to tackle the debts you listed out and set aside savings.

6. TRACK YOUR SPENDING

For a few months at least, track e v e r y t h i n g you spend. Chances are it’s just a few transactions a day. It shouldn’t take too long to write them down.

Make a note in your phone if that helps or leave a pen and paper on the fridge or just inside the door. Divide by category if you’re inclined or just write them all down. Doing this for a few months will give you more useful information than you’ve probably ever had about your spending habits. You will notice patterns and might be surprised. Maybe you’re spending hundreds of dollars eating out and didn’t even realize it! This will inform your budget going forward.

If you have never made a budget this might all seem like a lot! I get it.

It took me years of budgeting to get to the point where I knew every penny in and every penny out. It doesn’t need to take you years because there are so many wonderful resources available from people who went before you. If my plan doesn’t work for you, try someone else’s!! Anything that helps you get started is a win in my book. If you get paid every two weeks for 30 years, you have 780 chances to get things right.

Happy Budgeting.

Leave a Reply